Its generally recommended to shop around for new car insurance quotes after a major life event, such as entering college.

If you are attending school out-of-state, your car insurance premium could increase or decrease, depending on the average price in the new location. Additionally, your coverage needs might change. For example, if youre only planning to use your car a few times per month in college, you may feel comfortable dropping certain policies that arent required by your state.

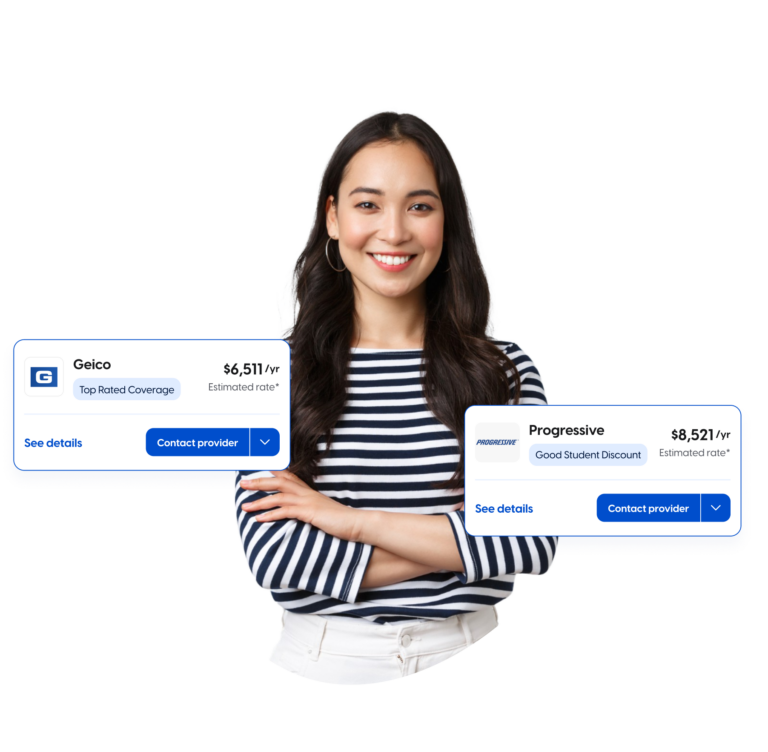

Another reason to shop around for car insurance quotes after starting college is because you might qualify for new discounts. Also, keep in mind that many car insurance companies provide a special discount to college students who leave their car at home and attend college more than 100 miles away. If a car is not essential on your campus, this is a good option to consider.