Call a licensed agent: 833-964-9663

Home » Car insurance » By age » When do car insurance rates go down?

Car insurance premiums are affected by a variety of factors, including your age. In general, teens and young adults pay the highest car insurance rates due to their lack of experience behind the wheel.

Rates usually fall rapidly each year for young drivers, but the decrease from year to year is less significant once a driver reaches their 30s.

Most drivers see the biggest savings on their car insurance premiums by age 25.

Why you can trust Rate Retriever

Our rates are based on public rate filings obtained by analytics company First Interpreter. While we may partner with some of the carriers you see on our site, we maintain editorial independence and it does not affect the rates you see. Read more about our rating methodology or see our rigorous editorial policy.

Our rates are based on public rate filings obtained by analytics company First Interpreter. While we may partner with some of the carriers you see on our site, we maintain editorial independence and it does not affect the rates you see. Read more about our rating methodology or see our rigorous editorial policy.

Last updated: August 8th, 2024

Car insurance premiums are affected by a variety of factors, including your age. In general, teens and young adults pay the highest car insurance rates due to their lack of experience behind the wheel and increased risk of accidents. Data shows that drivers between the ages of 16-19 have higher accident rates than any other age group.

If you’re like most young drivers, you might be wondering when does car insurance go down? In this guide, we’ll explain at what age car insurance goes down and highlight which insurance companies have the cheapest rates for young drivers.

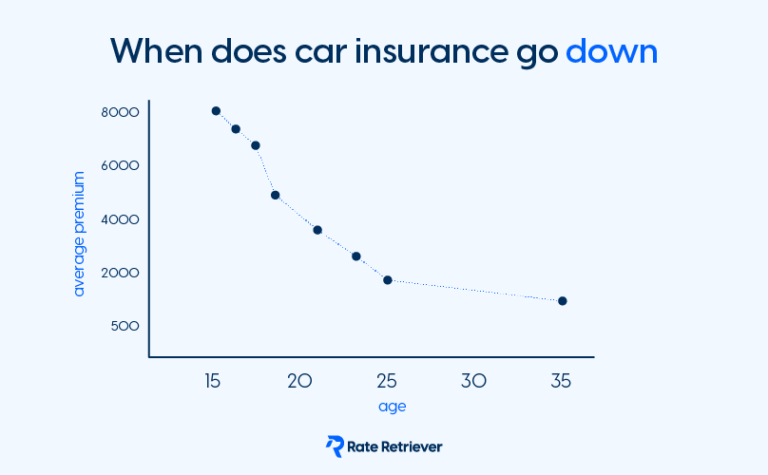

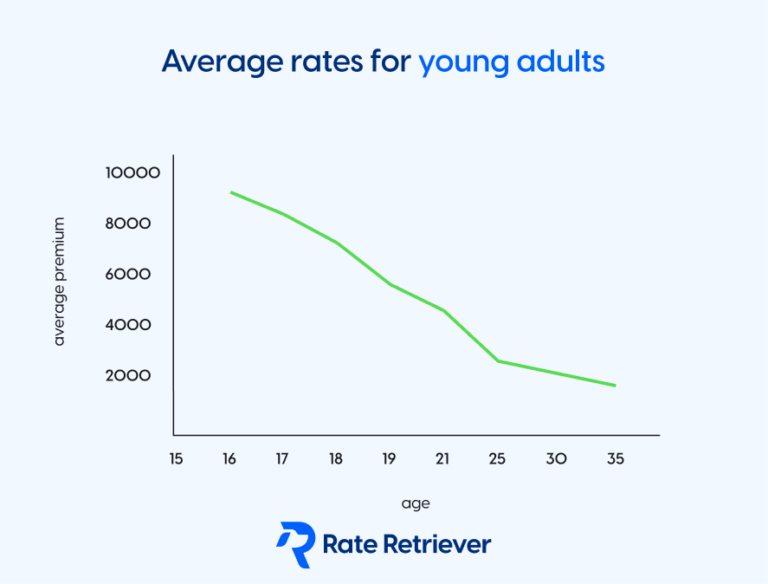

It’s a common belief that car insurance rates decrease around age 25. In many cases, car insurance rates actually start to go down earlier, around age 20.

However, most drivers see the most significant savings on their car insurance premiums by age 25. At this age, most drivers have almost a decade of driving experience and are less likely than younger drivers to get into accidents.

According to our rate data, the national average cost of car insurance at age 25 is $1,477 per year. For comparison, a single 17-year-old male on their own car insurance policy pays $4,058 for auto insurance, which is roughly $338 per month.

Once drivers reach their 20s, car insurance rates become more manageable. The average cost of car insurance for a 20-year-old driver is $2,752 and the average rate for a 23-year-old driver is $1,852. So, that means 25-year-olds pay about $1,280 less for car insurance than 20-year-olds.

In addition to your age, your car insurance company can also impact your rate. In the table below, you can see the average premiums for 25-year-old drivers from some of the top rated car insurance companies that offer insurance in a large portion of the US.

| State | Annual Premium |

|---|---|

| Alabama | 2,137 |

| Alaska | 1,971 |

| Arizona | 2,339 |

| Arkansas | 2,806 |

| California | 2,813 |

| Colorado | 2,801 |

| Connecticut | 2,910 |

| Delaware | 3,192 |

| Florida | 3,165 |

| Georgia | 2,922 |

| Hawaii | 1,376 |

| Idaho | 1,684 |

| Illinois | 2,498 |

| Indiana | 2,036 |

| Iowa | 2,163 |

| Kansas | 2,544 |

| Kentucky | 2,763 |

| Louisiana | 3,795 |

| Maine | 1,871 |

| Maryland | 3,221 |

| Massachusetts | 2,245 |

| Michigan | 3,436 |

| Minnesota | 2,629 |

| Mississippi | 2,114 |

| Missouri | 2,910 |

| Montana | 1,796 |

| Nebraska | 2,535 |

| Nevada | 3,407 |

| New Hampshire | 2,054 |

| New Jersey | 3,444 |

| New Mexico | 2,134 |

| New York | 4,830 |

| North Carolina | 1,963 |

| North Dakota | 2,186 |

| Ohio | 1,883 |

| Oklahoma | 3,002 |

| Oregon | 2,029 |

| Pennsylvania | 2,710 |

| Rhode Island | 2,794 |

| South Carolina | 2,262 |

| South Dakota | 2,836 |

| Tennessee | 2,288 |

| Texas | 2,915 |

| Utah | 2,461 |

| Vermont | 1,748 |

| Virginia | 2,147 |

| Washington | 2,324 |

| Washington DC | 3,043 |

| West Virginia | 2,132 |

| Wisconsin | 2,134 |

| Wyoming | 1,586 |

Annual rates estimated using search data from users ages 25-75 looking for full coverage car insurance. Rates do not represent actual quotes. Accurate as of July 2026.

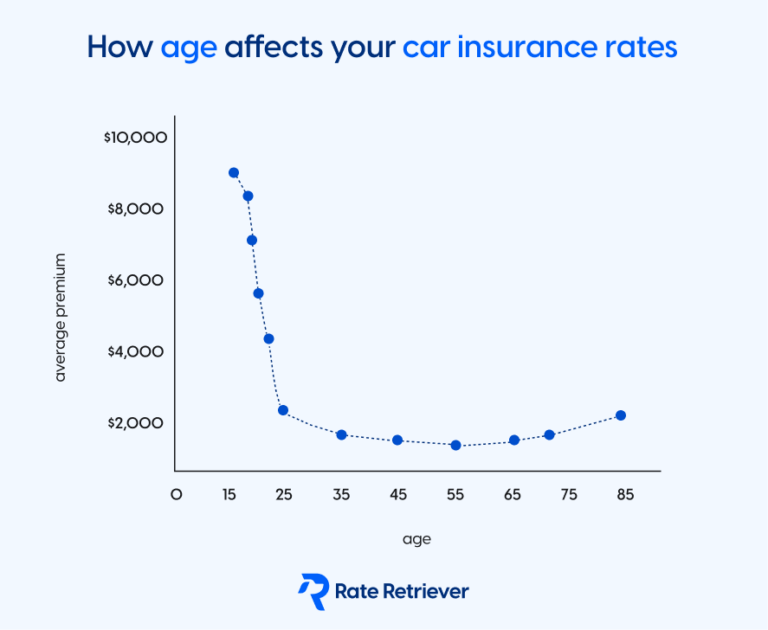

After age 25, car insurance premiums continue to drop for most drivers. Based on our rate data, a single 28-year-old male pays $1,421 for car insurance, which is only a decrease of $56 compared to the average rate for 25-year-olds. However, rates usually start to fall rapidly once a driver reaches their 30s.

The average premium for a 35-year-old is $1,294, the average rate for a 45-year-old is $1,252, the average rate for a 53-year-old is $1,186, and the average rate for a 65-year-old is $1,185.

Eventually, car insurance premiums start to increase again. On average, 72-year-olds pay $1,310 for car insurance and 80-year-olds pay $1,553. This is because older drivers have statistically higher fatal crash rates than drivers in some other age groups.

The main reason why car insurance rates go down around age 25 is that drivers are less risky to insure. Multiple studies indicate that drivers under 25 are more likely to get into car crashes than drivers in any other age demographic. The rates of injury and fatal accidents are also extremely high among drivers under 25.

Once a driver turns 25, their risk of accidents and insurance claims goes down. According to the National Safety Council (NSC), the overall accident rate per 100,000 licensed drivers decreases steadily as drivers age. Therefore, most insurance companies can charge drivers lower car insurance premiums as they get older.

In general, car insurance rates get cheaper with age, starting around age 20. But at a certain point, rates start to increase again. Data shows that car insurance premiums go down every year until age 70, when average rates start to go back up (but most seniors will not pay the same high rates they did as a young driver).

However, car insurance rates are not guaranteed to go down as drivers get older. Factors like your location, credit score, claim history, and driving record will always impact your rate, regardless of your age.

It’s possible that a 50-year-old driver with poor credit and several accidents on their record will pay more for car insurance than a 40-year-old with excellent credit and a clean driving record. Or, if you move to an area with a high risk of severe weather or a high vehicle theft rate, your car insurance premium could increase significantly, even when you’re older.

The best way to get the most affordable car insurance rate is to compare quotes. Comparing car insurance quotes makes it easy to see which insurer can offer you the lowest rate for your coverage needs and your current situation.

There is no definitive answer to, “What age does your car insurance go down.” For most drivers, car insurance rates are the lowest in their late 50s.

However, car insurance rates usually decrease steadily starting in your mid-20s, assuming you maintain a clean driving record, avoid insurance claims, and have good credit.

Regardless of your age, it’s important to get new car insurance rates on a semi-regular basis. Many insurance experts recommend getting updated rate quotes once per year, after a claim, or after a major life event, like moving or adding another driver to your policy.

While it’s true that car insurance rates tend to drop as you get older, there are many other factors that can cause your car insurance premium to go down. Here are some things that can result in a lower car insurance premium:

Your car insurance premium is largely dependent on where you live. If you move to a new city or state, your car insurance rate could come down.

Adjusting your coverage, like lowering your policy limits or dropping optional endorsements, can result in a cheaper premium.

If you have recent accidents or speeding tickets on your driving record, your premium will go down once those violations are removed.

Many car insurance companies offer discounts for good drivers, claim-free drivers, policy bundling, paying in full, taking a defensive driving course, and others, which can lower your rate.

Compare how much insurance costs at the top insurance companies near you

Quick | No Phone or Email Required | Reliable Results

"*" indicates required fields

Rate Retriever estimates average rates using the thousands of results we generated for our users over the last 18 months. These results include estimated quotes from our insurance carrier partners and additional estimates based on public rate filings.

For the data on this page, we analyzed searches from drivers ages 25-75 who were searching for full coverage car insurance. These rates are not actual quotes and should only be used for comparative purposes. Your rates can vary significantly based on your unique driver profile.

At Rate Retriever, our mission is to make the way you shop for insurance transparent and fair through user-friendly tools that respect your privacy and deliver reliable, comprehensive results.

So we took everything we hated about comparing insurance quotes online – the spam, the long questionnaires, the limited choices, the inaccuracy of quote prices – and threw it out the window, favoring a quicker form that more accurately estimates what you’ll pay at each of the top insurance providers near you.

Rate Retriever is an independent company that is not owned by an insurance provider, nor do we provide insurance ourselves. This independence allows us to be your free and impartial insurance research tool, helping you make the best decisions for your insurance needs.

We may earn a commission when you click one of the links, buy a policy, or call one of the providers listed on our site; however, we do not allow our partnerships to influence which information we provide in our guides.