Call a licensed agent: 833-964-9663

Homeowners insurance helps protect the physical structure of your home, your personal belongings, and your liabilities in the case of a covered peril. Most mortgage lenders require you to have a home insurance policy, but it’s often a good idea even if it’s not required.

No phone or email required. Seriously.

Homeowners insurance is a policy that protects the physical structure of your home, your personal belongings, and your liabilities. If your home or personal items get damaged in a covered loss, your insurance company reimburses you for the cost of repairs. It also pays to rebuild your home if your house gets destroyed in a covered peril. Read more.

Start saving on your homeowners insurance now

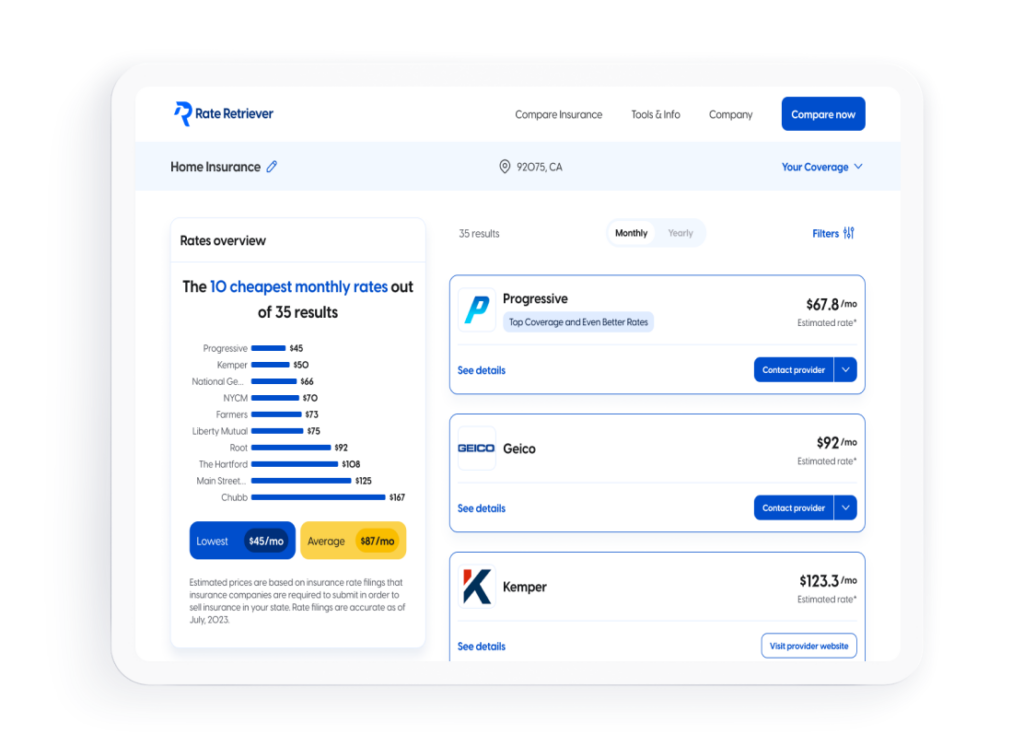

Based on your answers to our short quiz, we’ll estimate how much your home insurance will cost at each of the top providers near you, so you can find the coverage you need at a price you can afford.

Start comparing in only 1-2 minutes

We don’t require your phone number or email to see your results

Personalized rate estimates calculated using the insurance company’s rating plan (plus any applicable discounts)

Read our spam-free promise

Why you can trust Rate Retriever

Our rates are based on public rate filings obtained by analytics company First Interpreter. While we may partner with some of the carriers you see on our site, we maintain editorial independence and it does not affect the rates you see. Read more about our rating methodology or see our rigorous editorial policy.

Our rates are based on public rate filings obtained by analytics company First Interpreter. While we may partner with some of the carriers you see on our site, we maintain editorial independence and it does not affect the rates you see. Read more about our rating methodology or see our rigorous editorial policy.

Some of the best home insurance companies on the market are Amica, Allstate, State Farm, Nationwide, and USAA. But while these companies are some of the largest insurers with the highest ratings, the best home insurance company depends on your unique circumstances.

When shopping for home insurance, it’s important to consider your location, the type of home you live in, and your coverage needs. You should also compare home insurance quotes to find the most affordable policy for your situation.

Home insurance is not required by law. However, most mortgage lenders require it as part of a loan agreement. Having homeowners insurance provides financial protection for the lender in case something happens to your home before your loan is paid off.

But even if you are not required to have home insurance, it’s still a good idea to purchase coverage. Without home insurance, you are financially responsible for anything that might happen to your home or personal belongings.

Home insurance is a package policy. There are a few types of coverage that are included in most standard policies:

Dwelling insurance protects the physical structure of your home and attached structures, such as a garage, porch, or deck.

Personal property insurance covers personal belongings, such as furniture, clothing, and electronics. It also covers items in your vehicle.

Personal liability insurance covers your financial responsibilities if someone gets injured on your property, or if you accidentally damage someone else’s property.

Medical payments insurance pays for the medical bills of someone that gets injured on your property, even if you were not responsible.

Additional living expenses (also called loss of use) covers the cost of temporary housing, restaurant meals, parking fees, and laundry if your home is damaged in a covered loss and you have to relocate while it gets repaired.

A standard home insurance policy includes multiple types of coverage. It includes coverage for the structure of your home, your personal possessions, personal liabilities, medical payments for injuries, and additional living expenses.

Additionally, home insurance policies either provide coverage for named perils or open perils. Named perils are specific losses that are listed in your policy. They typically include:

The alternative to a named perils policy is an open perils policy. With an open perils policy, your dwelling and personal items are protected against any losses that are not explicitly excluded from the wording of your policy documents.

Home insurance rates are different for every property owner. However, there are plenty of ways to save money on home insurance coverage. Here are some tips for getting a lower rate:

Many insurance companies offer discounts for things like having a new home, getting a quote in advance of your policy’s start date, and signing up for automatic payments.

Bundling your auto and home insurance policies with the same insurer often results in a discount.

The best car insurance company is different for every driver. It depends on your coverage needs, what discounts you can qualify for, your budget, and what you value in an insurance company. To find the best car insurance company, research several insurers that meet your coverage needs, then get quotes to find the most affordable policy for you.

Most insurance companies give discounts to customers who pay their annual premiums in full rather than in monthly installments though the year.

Customers with no auto or home insurance claims on their record often get a small discount on their premium.

Before you purchase homeowners insurance, it’s a good idea to compare home insurance quotes. Follow these steps to compare prices:

Look into several insurance companies that sell coverage in your area. Read customer reviews and check third-party ratings to make sure they are a reliable and trustworthy provider.

Consider factors such as the value of your home, your location, and the value of your personal belongings. If you want high coverage limits or special endorsements, make sure to choose an insurer that offers the coverage you want.

Contact several insurance companies and request quotes based on your coverage needs. Many home insurance providers allow you to get an instant quote online.

Review the quotes you received and see which company can offer you the lowest rate. However, make sure to choose a carrier that meets all of your needs. The cheapest company isn’t necessarily the best one.