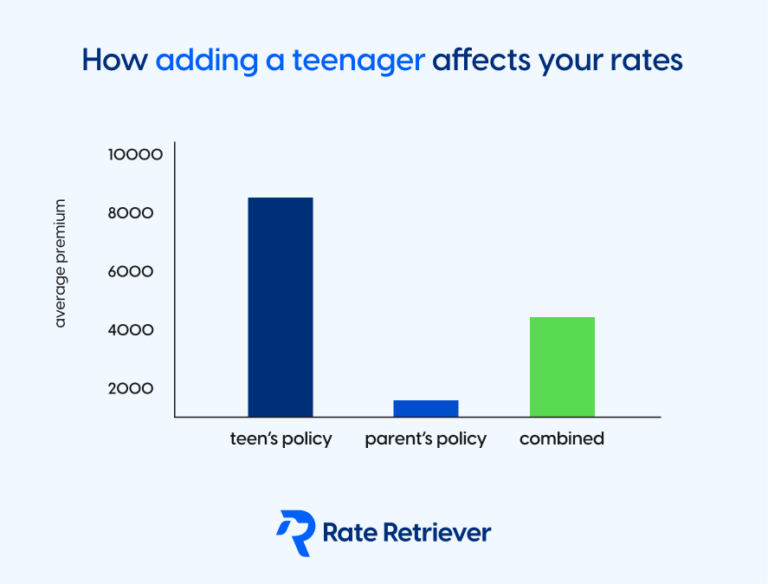

You generally need to add your teen to your car insurance policy when they get their driver’s license; although your state or car insurance company may require you to add your teen when they have their learner’s permit. If your teen will be driving your car regularly, most insurance companies require them to be added to your policy. It’s always best to discuss your specific situation with your insurance agent to determine the best course of action.