Call a licensed agent: 833-964-9663

Car insurance rates are personalized for every driver. But depending on factors like your location and driving record, car insurance premiums can be extremely expensive. There are many reasons why car insurance rates can be costly, but the good news is that car insurance rates often decrease with age, assuming you avoid accidents and claims.

In this guide, we’ll discuss how car insurance companies determine rates and explain why is car insurance so expensive in 2023. Understanding how car insurance premiums work and how they’re calculated can also help you save money on your policy.

Our rates are based on real results quoted to past users in the last 18 months. While we may partner with some of the carriers you see on our site, we maintain editorial independence and it does not affect the rates you see. Read more about our rating methodology or see our rigorous editorial policy.

If you’re wondering, “Why is car insurance so expensive,” you’re not the only one. Multiple studies have shown that car insurance rates have increased in recent years.

However, that’s not to say that car insurance is expensive for everyone. When you apply for an auto insurance policy, the insurance company looks at a variety of different factors to calculate your customized premium. These factors include both external factors and personal factors.

Auto insurance rates have been increasing across the board for several reasons that affect most people. These include:

When one or more of these things happen, it makes it more expensive for insurance providers to insure you. For example, when there is a natural disaster, there can be a huge spike in the amount of people making an insurance claim at the same time. When there are more frequent natural disasters, it becomes very expensive for insurance companies that are usually better equipped to handle a lower percentage of claims at one time.

To combat external factors like inflation and natural disasters, insurance companies will try to raise their rates across the board. Insurance providers do this by updating their rating plan, which must be approved by your state. Once the rating plan is approved, the company can raise their rates.

Other factors that impact your car insurance rate include:

While some of these factors are out of your control, like inflation, you can control other factors. For instance, drivers with excellent credit tend to pay lower rates for car insurance. If your credit score is low, raising your score could help you lock in a more affordable premium.

If you’re paying a high car insurance rate right now, it probably won’t be this expensive forever.

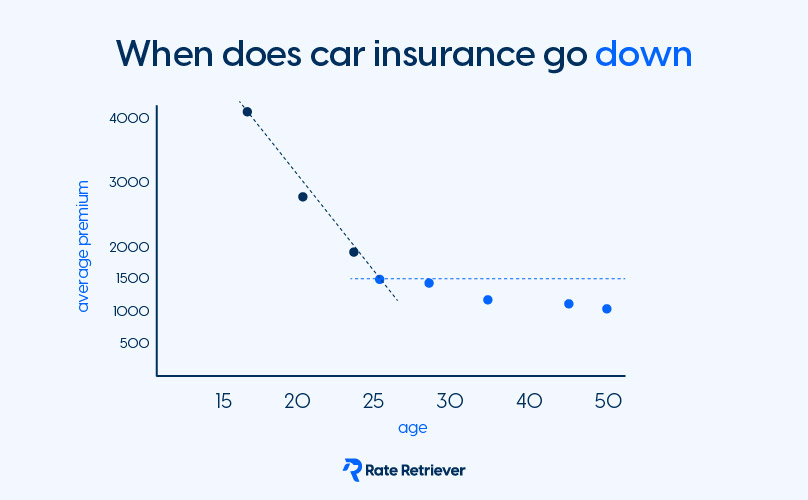

For most drivers, car insurance premiums start to decrease with age. Because young drivers often pay the highest rates, you can expect your premium to drop as you get older. In addition, changes in your driving record can positively impact your rate.

For example, if you have several speeding tickets or accidents on your record, those violations will eventually get removed, usually after a few years. Once those violations are dropped, your car insurance premium should get less expensive.

However, it’s important to know that your car insurance premium is not guaranteed to get cheaper over time. While rates typically decrease with age, there are other factors at play that could prevent your rate from dropping (like a problematic driving record).

Young drivers under the age of 25 often pay the highest car insurance rates. This is because newly licensed drivers lack experience behind the wheel. Statistically, drivers between the ages of 16–19 have higher crash rates than any other age group. Young drivers are also more likely to make mistakes that can lead to serious accidents.

Due to the increased risk of accidents and other car insurance claims, insurance companies generally charge young adults the most expensive rates. However, data shows that car insurance premiums tend to start decreasing around age 25. This is assuming drivers maintain a clean driving record and have no prior claims.

You might have heard that the color of your vehicle impacts the cost of your car insurance. Specifically, it’s believed that red cars are more expensive to insure. However, there’s no truth to this—it’s only a myth.

There are lots of factors that affect your car insurance premium, but the color of your car is not one of them. Whether you own a red car, white car, or black car, your car insurance premium will be the same.

However, the make, model, and year of your vehicle can impact the cost of your car insurance policy. For instance, if you own a 2023 Honda Civic, the cost of your car insurance will probably be higher than the cost of insurance for a 2015 Honda Civic.

If you think you’re overpaying for auto insurance, there are ways to get a cheaper car insurance premium. Here are a few strategies that could help you save money:

Compare how much insurance costs at the top insurance companies near you

Quick | No Phone or Email Required | Reliable Results

"*" indicates required fields