Call a licensed agent: 833-964-9663

In most states, people with Poor credit scores pay more for car insurance than those with Good credit.

If you have a lower credit score, applying for non-standard insurance may be the cheapest option. The General, National General, and Dairyland are a few insurance companies that offer non-standard insurance options.

Our rates are based on real results quoted to past users in the last 18 months. While we may partner with some of the carriers you see on our site, we maintain editorial independence and it does not affect the rates you see. Read more about our rating methodology or see our rigorous editorial policy.

There are many factors that impact your car insurance rates, but one of the biggest is your credit score.

In most states, car insurance companies are allowed to use your credit score as a rating factor when they calculate your premium. In general, drivers with good credit pay lower rates for car insurance, while drivers with poor credit pay higher rates.

If you don’t have perfect credit, however, there are still ways to get a more affordable policy. In this article, we’ll explain how credit impacts the cost of car insurance, and how you can get cheaper car insurance with bad credit.

Car insurance premiums are often impacted by your credit score, in addition to many other factors such as your location, age, and driving record. The better your credit is, the lower your premium usually is.

Here’s a look at the credit tiers and the credit score ranges associated with each:

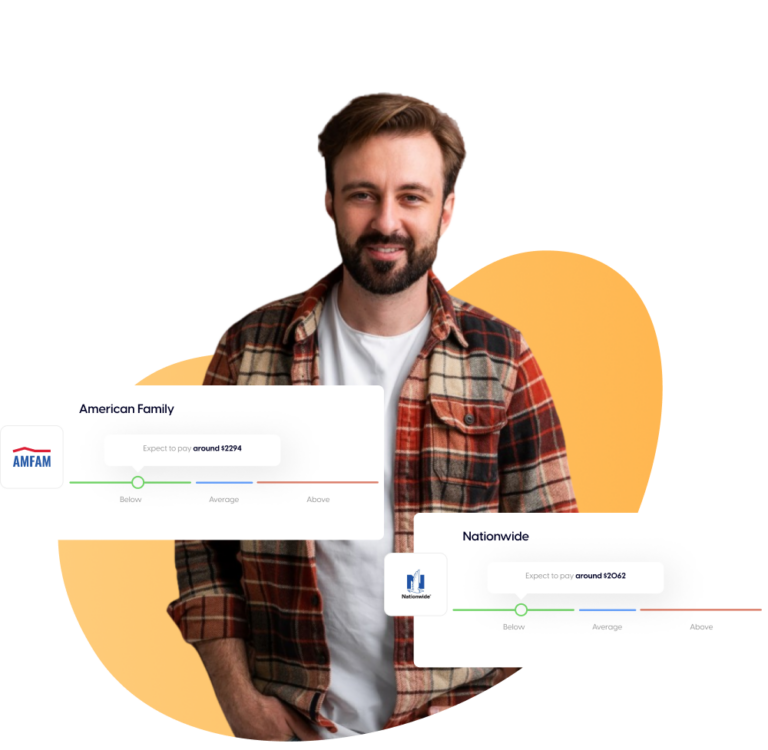

On average, a 35-year-old male driver with excellent credit will pay one price for car insurance, while the average rate for the same driver with good credit will be a little more. Drivers with poor credit pay the highest rate on average.

Your credit score is often used as an insurance rating factor because it helps determine risk. According to the Insurance Information Institute (Triple-I), your credit score is used to predict the likelihood of losses, like an accident or physical damage claim. Statistically, drivers with bad credit are more likely to experience insurance losses, and therefore, pay higher rates.

Not all states used credit-based insurance scores. In a handful of states, this practice is limited or banned. The following states prohibit the use of credit-based insurance scores:

If you live in one of these states, auto insurance companies cannot use your credit score to determine the rate you pay for a policy. Whether you have excellent credit or poor credit, your score will not impact your rate. However, that means other rating factors, like ZIP code, age, vehicle type, and driving record could hold more weight.

In Maryland and Michigan, the use of credit score in insurance is limited, meaning insurance companies may not be allowed to use credit score as a reason to drop or refuse to write or renew your policy.

It’s possible to get denied car insurance due to your credit history if your state allows the use of credit-based insurance scores. If you have very low credit, you might find that some insurance companies are unwilling to issue you a policy. The only way to know whether you can get approved for car insurance with bad credit is to apply.

If you have bad credit, you might consider looking into non-standard car insurance companies. These providers specialize in insuring high-risk drivers, including drivers with poor credit or criminal offenses, like a DUI. These carriers tend to have more flexible eligibility requirements and will often cover drivers with bad credit.

Yes, it’s possible to get auto insurance with a credit score of 500. However, a credit score of 500 falls into the “poor” credit tier. In this case, you should consider applying for non-standard car insurance, which can make it easier to get approved. Providers such as The General, National General, Dairyland, Bristol West, Safe Auto, and Kemper offer non-standard auto insurance.

While having bad credit doesn’t necessarily disqualify you from purchasing coverage, it will impact your rate. If your credit score is 500, you can expect to pay a higher rate for coverage than you would if your score was in the “fair” or “good” tier. In addition, non-standard insurance companies often have higher premiums because most drivers insured by that company are also considered high-risk.

Having poor credit usually results in a more expensive car insurance premium. However, it’s possible to get cheap car insurance for bad credit.

As you’re researching insurance companies, look for providers that offer discounts you qualify for. Many carriers offer savings for policy bundling, taking a defensive driver course, paying in full, and having safety features in your car, like an anti-theft device.

You can also consider choosing higher deductibles when you purchase your policy. Certain types of coverage, like collision and comprehensive insurance, require a deductible when you have a claim. By selecting a higher deductible, you will lock in a lower monthly premium.

Another way to lower your premium is to improve your credit score. If you can boost your credit enough to land in a higher credit tier, you could see big savings on your policy after the renewal period.

The best car insurance for bad credit depends on many different factors, including your location, age, driving record, and coverage needs. To find the best insurer for you, take our short quiz to see what you can expect to pay at top insurance companies near you. Just answer a few questions and see your rates.

Compare how much insurance costs at the top insurance companies near you

Quick | No Phone or Email Required | Reliable Results

"*" indicates required fields