What car insurance coverage is right for you?

![]() Alyssa DiCrasto

on

2024-09-12

Alyssa DiCrasto

on

2024-09-12

What car insurance coverage is right for you?

Written by Katie Dee

Edited by Alyssa DiCrasto

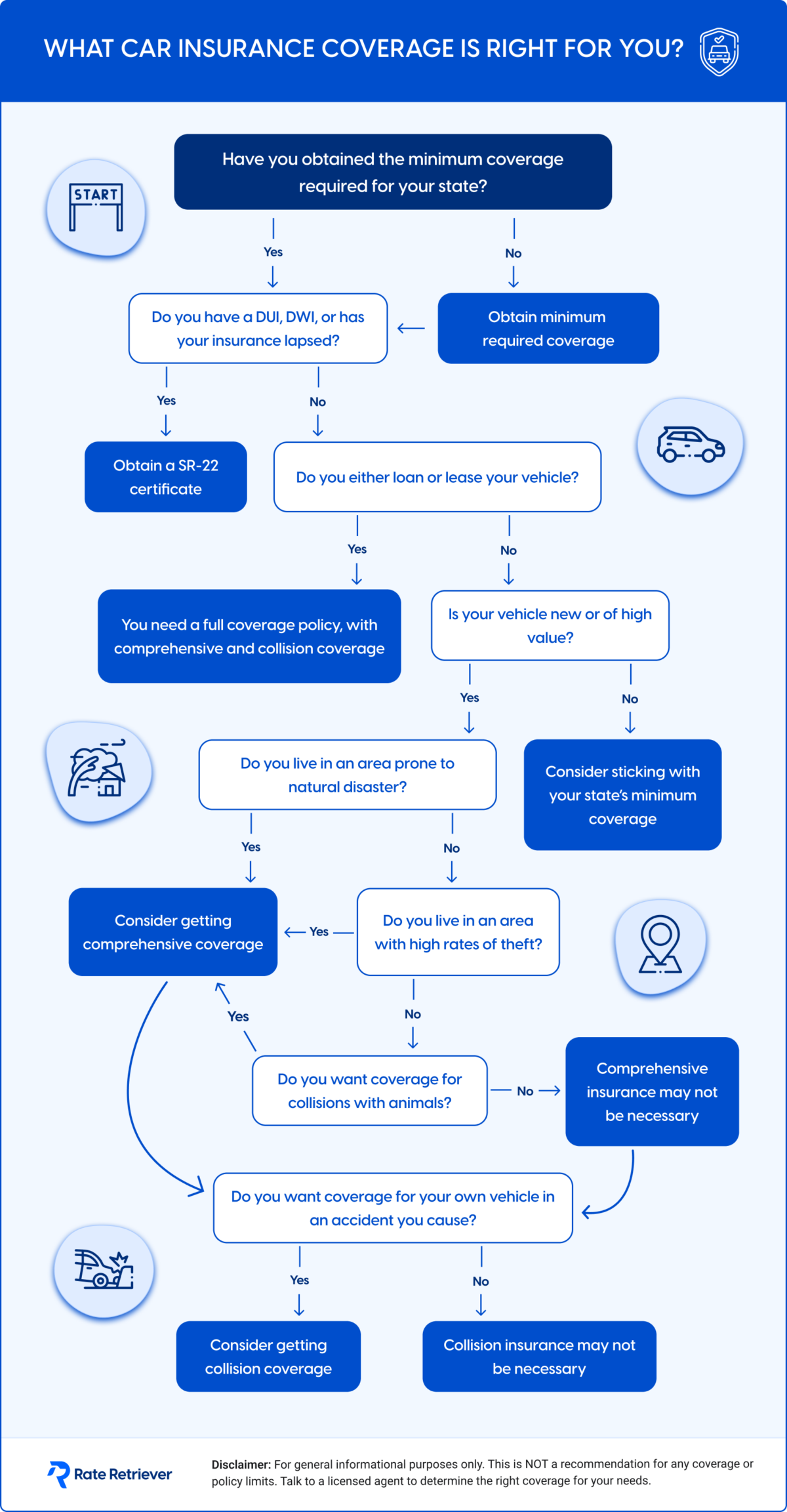

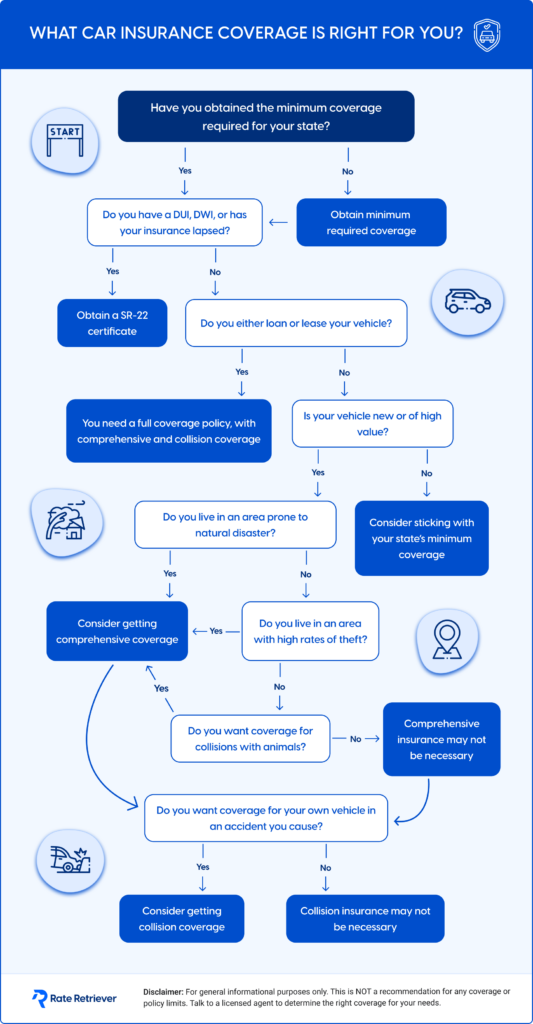

Finding the coverage you need

When it comes to car insurance, finding the right coverage can feel overwhelming. With so many options, it’s important to make sure you’re adequately protected without overpaying for coverage you don’t need. Whether you’re a new driver or simply reassessing your current policy, choosing the right car insurance is about understanding your personal situation and risk factors.

To make the process easier, we’ve created a simple flowchart that guides you step-by-step toward the coverage that’s right for you. Just follow along, and by the end, you’ll have a clearer idea of what you need. Let’s get started!

Find cheap car insurance near you

Frequently asked

What factors affect your car insurance rates?

Does your lifestyle affect your car insurance?

How does where you live influence the cost of auto insurance?

About Rate Retriever

At Rate Retriever, our mission is to make the way you shop for insurance transparent and fair through user-friendly tools that respect your privacy and deliver reliable, comprehensive results.

So we took everything we hated about comparing insurance quotes online – the spam, the long questionnaires, the limited choices, the inaccuracy of quote prices – and threw it out the window, favoring a short form that more accurately estimates what you’ll pay at each of the top insurance providers near you.

Rate Retriever is an independent company that is not owned by an insurance provider, nor do we provide insurance ourselves. This independence allows us to be your free and impartial insurance research tool, helping you make the best decisions for your insurance needs.

We may earn a commission when you click one of the links or call one of the providers listed on our site; however, we do not allow our partnerships to influence which information we provide.

Share this article