2023 vs. 2024 Insurance Rates

Call a licensed agent: 833-964-9663

![]() Kelsie Johnson

on

2024-07-18

Kelsie Johnson

on

2024-07-18

Home » Archives for Kelsie Johnson

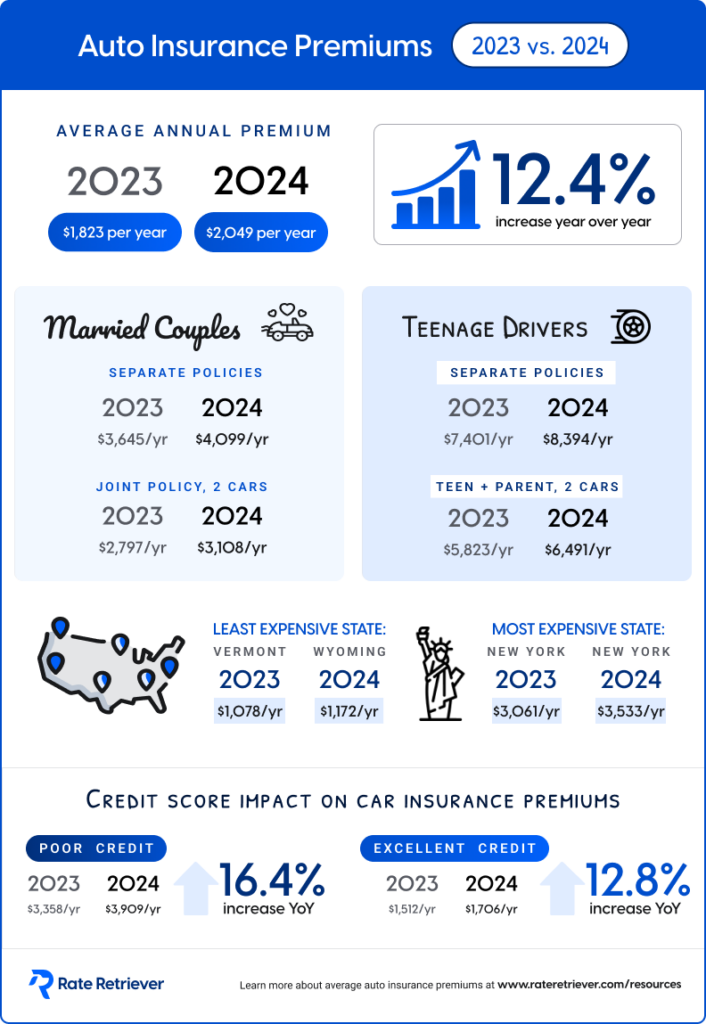

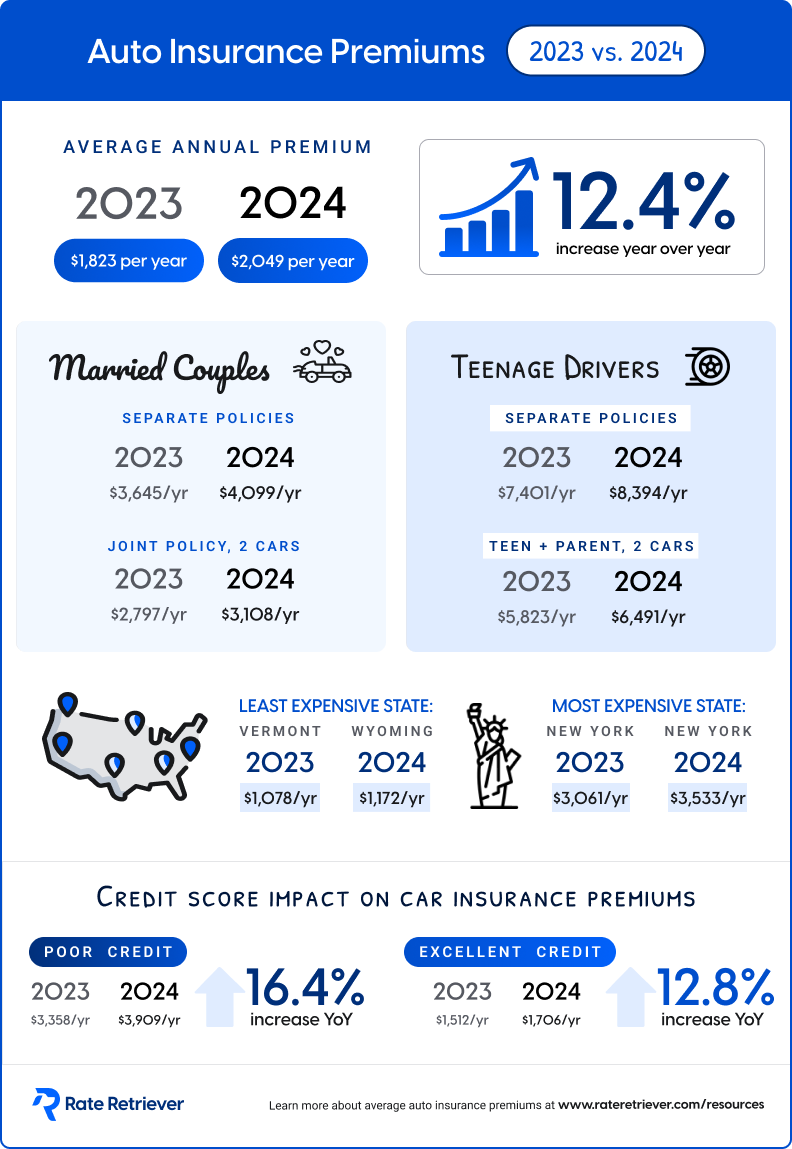

Have you noticed your car insurance rates going up lately? It’s not just you—many drivers have seen their premiums increase significantly over the past year. Today, the average cost of car insurance sits at a whopping $2,049 per year, a 12.4% increase from 2023 when the national average was an estimated $1,823 annually.

But that’s not all that has changed. The least expensive state to insure a vehicle also looks different this year than it did last year. In 2023, the cheapest state for car insurance was Vermont, with an average annual premium of $1,078. However, in 2024, the cheapest state is Wyoming with an annual premium of $1,172.

Several factors have contributed to this rise in rates. Firstly, insurance always lags behind the rate of inflation. This means that in the wake of high inflation, insurance rates will follow suit. Second, the cost of repairing vehicles has escalated with the advancement of car technology. Newer cars tend to have more sophisticated features, which can make repairs pricier. Lastly, severe weather events are occurring more frequently. This increases the likelihood that a policyholder will file a claim due to weather damage, and thus, increases the financial risk for insurance companies.

Knowing how quickly insurance rates can change, it’s always wise to keep an eye on your insurance premiums and periodically shop around to compare quotes. Staying on top of your rates and comparison shopping could help you to find a better deal at a new provider that works with your current driving habits and budget.

![]() Kelsie Johnson

on

2024-07-12

Kelsie Johnson

on

2024-07-12

There are a few ways to purchase car insurance. Learn the differences between a captive agent, independent agent, and broker, and see the pros and cons of each.

![]() Kelsie Johnson

on

2024-07-12

Kelsie Johnson

on

2024-07-12

Moving to a new state can affect your auto insurance requirements and costs. Here’s what you need to know about car insurance when moving to a different state.

![]() Kelsie Johnson

on

2024-07-12

Kelsie Johnson

on

2024-07-12

Many car insurance companies offer discounts to help drivers save money. See the most common car insurance discounts and other ways to lower your rate.

![]() Kelsie Johnson

on

2024-05-23

Kelsie Johnson

on

2024-05-23

Home » Archives for Kelsie Johnson

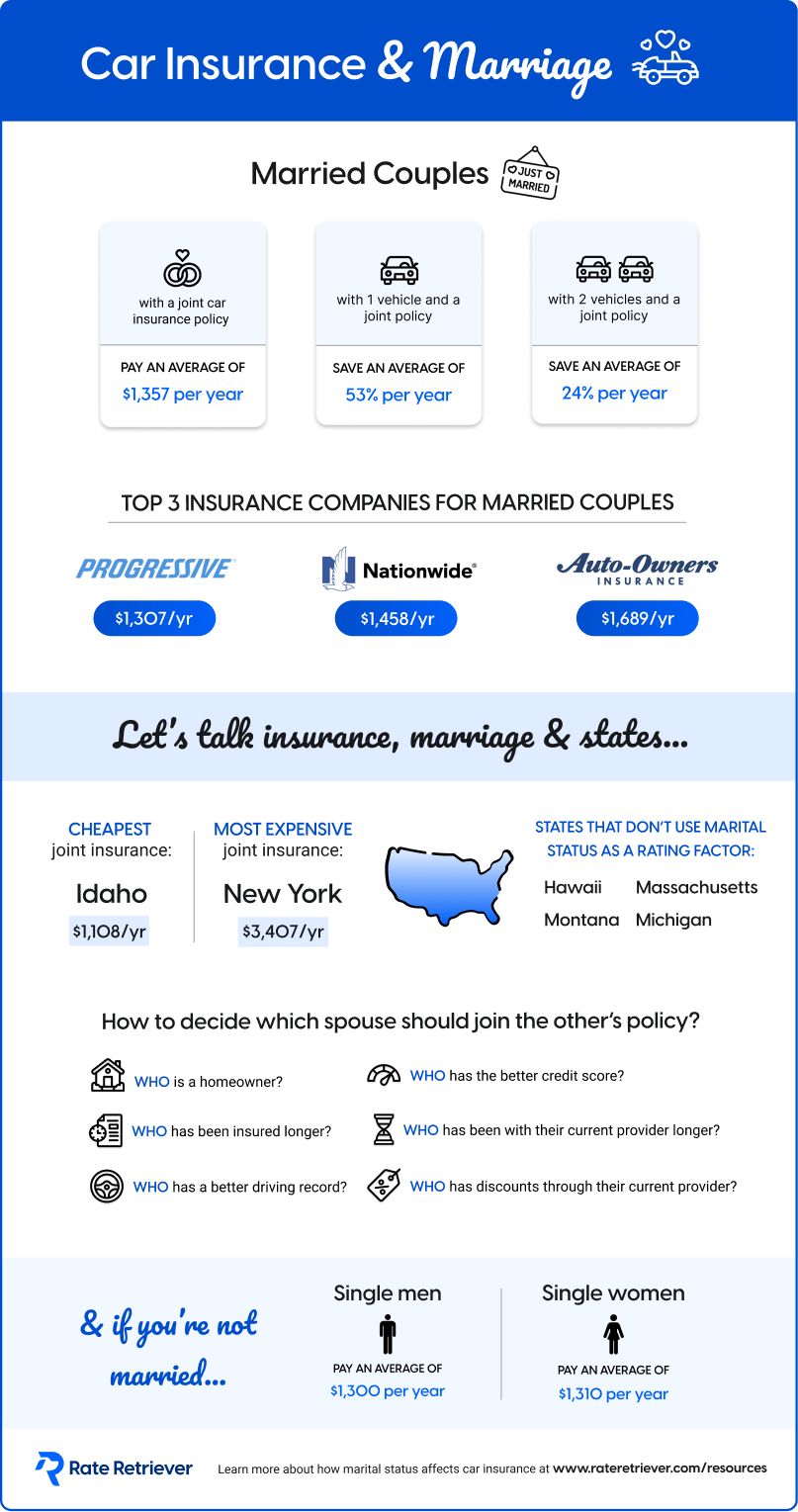

Embarking on the journey of marriage doesn’t just mean sharing a life together—it also means sharing in the perks, including surprising savings on car insurance. Rate Retriever’s research has shown that tying the knot can lead to discounts of up to 53% on auto insurance premiums.

Why the significant savings? Insurance companies often view married couples as lower risk, attributing it to a variety of factors such as shared financial responsibilities, stability, and statistically safer driving habits compared to single individuals.

So, as you exchange vows and start your journey as a married couple, don’t forget to double check your car insurance rates. According to our research, the cheapest national company for married couples in 2024 is Progressive, with an average annual premium of just $1,307, and Nationwide and Auto-Owners Insurance not far behind.

The amount of savings you achieve will – of course – depend on several factors including how many cars are on your policy, the state you live in, and the auto insurance company you are working with. It is also important to remember that not every state takes marital status into account while setting rates.

Be sure to keep your car insurance company in the loop about this exciting life change and you may end up saving big because of it!

![]() Kelsie Johnson

on

2024-05-15

Kelsie Johnson

on

2024-05-15

Home » Archives for Kelsie Johnson

Read time: 3 min

For homeowners, having a comprehensive home insurance policy is essential. It provides valuable protection in case your home gets damaged or destroyed in a covered event, like a windstorm, fire, or break-in. It also covers your personal items, liability, loss of use, and more.

One of the most common questions that homeowners have about home insurance is how it differs from hazard insurance. Home insurance and hazard insurance are related but they aren’t exactly the same. In this guide, we’ll explain the difference between hazard insurance vs. home insurance.

Home insurance is a bundle of policies that cover your home and your personal items. A typical homeowners insurance policy includes dwelling insurance, personal property insurance, liability insurance, medical payments insurance, and loss of use insurance.

Hazard insurance, on the other hand, only covers the physical structure of your home. Hazard insurance is the same thing as dwelling insurance, and it’s included with every home insurance policy.

Hazard insurance is not the same thing as home insurance. However, hazard insurance is a part of your homeowners insurance policy. When you purchase a basic home insurance policy, it automatically includes hazard insurance, which is more commonly called dwelling insurance.

The main difference between hazard insurance and home insurance is what’s covered. Hazard insurance only covers the physical structure of your home, and attached structures, like a garage. It doesn’t cover your personal items or your liabilities.

Homeowners insurance is a package of policies that protects more than just the physical structure of your home. The hazard insurance portion will cover your house, but you also get coverage for personal property, personal liability, guest medical payments, and loss of use.

Every homeowner can benefit from having home insurance. If you have a mortgage, most lenders require homeowners to carry a standard homeowners insurance policy that includes hazard insurance.

If the physical structure of your home gets damaged in a covered peril, you will file a claim under your hazard insurance. Once the claim is investigated and approved, you will receive a payout for the estimated cost of repairs.

Without hazard insurance, you would have to pay to repair or rebuild your home entirely out-of-pocket.

Home insurance is essential for every homeowner. You probably need home insurance to satisfy your lender’s requirements, but it also provides peace of mind.

Home insurance covers a variety of risks that you can face as a homeowner, including damage to the structure of your home, damage to personal items, third-party liability claims, guest injuries, and temporary living expenses if your home gets damaged or destroyed.

If you want to file a personal liability claim, personal property claim, medical payments claim, or loss of use claim, you need to have home insurance. Hazard insurance will only cover claims related to structural home damage.

Hazard insurance covers the physical structure of your house. It also covers structures attached to your home, like a garage or porch. It covers features like the walls, roof, ceiling, and foundation, as well as major home systems, like HVAC and plumbing, and permanent fixtures, like cabinets and large appliances.

Depending on your home insurance policy, your hazard insurance will either cover named perils or open perils. Named perils are specific losses that are listed in your policy. Open perils means that you are covered against any loss that is not explicitly excluded in your policy.

Some of the most common perils that hazard insurance will cover include:

Keep in mind that hazard insurance almost never covers damage from earthquakes or flooding, even if you have an open perils policy. If you live in an area that is prone to earthquakes or floods, it’s a good idea to purchase separate earthquake insurance and flood insurance policies.

There are a variety of ways for homeowners to save money on their home insurance policies. Here are some tips for getting a lower premium:

Most mortgage lenders require homeowners to have hazard insurance. This protects the lender’s financial interest in your home before it’s paid off. Before you close on your home, your lender will ask to see proof of home insurance with hazard coverage. If you file a hazard insurance claim, the mortgage lender is typically responsible for holding the money to ensure that the proper repairs are made to their standards.

Another name for hazard insurance is dwelling insurance, which is more commonly used. Hazard insurance and dwelling insurance may be used interchangeably since they reference the same thing.

Hazard insurance is a type of insurance that covers the physical structure of your home, as well as the roof and foundation. Hazard insurance also covers attached structures, major home systems, and permanent interior features, like cabinets, flooring, walls, and large appliances. Hazard insurance is included with every standard home insurance policy.

![]() Kelsie Johnson

on

2024-04-17

Kelsie Johnson

on

2024-04-17

Read time: 3 min

In Georgia, car insurance companies are allowed to use credit-based insurance scores. That means your credit score can have a direct impact on the cost of your auto insurance policy. In general, Georgia drivers with bad credit pay higher rates for coverage. Drivers with good credit often pay lower insurance premiums because they pose less risk.

No matter your personal credit score, it’s important to understand how your credit may impact your car insurance premium in Georgia. In this guide, we’ll discuss car insurance by credit score in Georgia and share average premiums from some of the best companies in the state.

Your credit score can have a significant impact on the cost of car insurance in Georgia. According to our recent rate data, the average annual cost of auto insurance in Georgia is $1,897. Drivers with excellent credit pay about 22% less than the statewide average, whereas drivers with poor credit pay nearly 68% more than the statewide average rate.

For example, in the beginning of 2024, the average cost of full coverage car insurance for a Georgia driver with excellent credit is $1,485 per year. For a driver with good credit, the average premium is $1,995 per year. Georgia drivers with bad credit pay an average of $3,191 per year.

The main reason why credit score impacts car insurance rates in Georgia is because it’s an indicator of risk. From an insurance company’s perspective, people with poor credit are riskier to insure and are more likely to file claims. To offset that increased risk, insurers charge higher rates for drivers with bad credit.

While Georgia car insurance companies are allowed to use credit-based insurance scores, not every state allows this. For example, in California, Hawaii, Maryland, and Massachusetts, car insurance companies are banned from considering a driver’s credit score when calculating their premium. A handful of other states prohibit insurers from charging higher rates to drivers that have no credit history.

Georgia drivers with bad credit can expect to pay above-average rates for car insurance. However, credit is only one factor that can affect premiums. Your ZIP code, age, driving record, and vehicle type are some of the other factors that can affect the cost of auto insurance.

In addition, the insurance company you choose can also impact how much you’ll pay. Based on our analysis of recent rate data, we found that Nationwide is the cheapest provider for drivers with poor credit and USAA is the cheapest for drivers with good credit.

If you have poor credit, there are plenty of ways to lower your car insurance premium. Here are some tips for finding the cheapest coverage if you have bad credit in Georgia:

Another way to find affordable car insurance in Georgia is to shop around. Comparing quotes from several insurance companies can help you find the cheapest policy for your situation, credit score, and coverage needs. If your credit score improves, it’s a good idea to re-shop for insurance quotes to see if you can find a better rate from a different carrier.

To find cheap car insurance in Georgia, you can use our online quote comparison tool.

There is no specific credit score that is needed to get car insurance. However, your credit score can impact how expensive your car insurance premium is in Georgia (and in most other states). Drivers with good credit usually pay the lowest rates for insurance because they are less risky to insure. People with bad credit are often assigned higher rates. If you improve your credit score, you can usually secure a lower monthly car insurance premium.

The average annual cost of car insurance in Georgia is $1,884, which is less than the U.S. national average rate of $2,049 per year. There are a few reasons why the cost of car insurance in Georgia is higher than in some other states. For instance, Georgia has a very high population density and it has some unique weather risks, like hurricanes. Additionally, Georgia is ranked 10th in the U.S. for states with the highest number of vehicle thefts.

Car insurance companies determine how much they charge you based on your driver profile. Factors that can impact your rates include:

Read more about the factors that impact your car insurance rate

Switching your car insurance is easy, even if you are in the middle of your current policy.

Here are some helpful tips to consider to switch your car insurance:

The answer to this question depends on where you live and what you would like to cover.

Each state has its own minimum requirements on the type and amount of insurance needed. When you’re trying to determine what and how much car insurance you need, you can start by reviewing your state’s requirements.

Find out what’s required in your state

Once you review your state’s minimum requirements, you may find that you want additional coverage. For example, sometimes owners of new cars want comprehensive coverage to insure their car from natural disasters and vandalism, even though comprehensive coverage isn’t required by their state. To figure out what insurance you want, you can review the different types of insurance to decide what makes the most sense for your situation.

The biggest difference between Rate Retriever and other comparison sites is that we are a free and impartial research tool NOT an insurance marketplace. This means you can’t purchase a policy directly through RateRetriever.com, but you can use our tool to independently research your options and seamlessly connect with the provider you choose.

Unlike other insurance comparison sites, we:

We like to think that Rate Retriever is your insurance companion, not just another insurance comparison site. Our values guide everything we do, which is why we strive to offer transparent, trustworthy insurance tools.

There are many ways you can try to get cheaper car insurance. The first is simply to get quotes from multiple providers. This will help you determine if you’re currently receiving the cheapest rates based on your needs and driver profile. Rate Retriever makes the comparison process easy.

Sometimes, the reason your car insurance is so expensive is due to your driver profile. For example, drivers under 20 years old usually pay more for insurance than more experienced drivers, and drivers with a recent at-fault accident or traffic violation typically pay more.

There are ways to lower the cost of your insurance such as taking a defensive driving course. Check with your provider to see if there are any discounts you qualify for or can reasonably earn.

Rate Retriever works with national and local insurance providers to provide our users with a seamless insurance shopping experience. We may earn a commission from our insurance provider partners when you click on a link, call, or purchase a policy from one of the providers listed on our site. That said, we’re committed to providing you with accurate, bias-free information, and we do not allow our partnerships to limit the results or influence the information we share with you.

We do not sell your personal information, charge you for using our tools, or sell you insurance policies. Additionally, should you choose to purchase a policy from one of our partners, the price you pay will not be adversely affected.

![]() Kelsie Johnson

on

2024-04-17

Kelsie Johnson

on

2024-04-17

Read time: 3 min

Car insurance is a legal requirement for all vehicle owners in Georgia. However, the cost of auto insurance in the Peach State is different for every driver. Car insurance companies consider lots of criteria to calculate your unique premium, and your age is one of the most notable factors.

If you’re in the market for car insurance, it’s helpful to understand how age can impact the cost of your coverage. In this guide, we’ll look at age and car insurance in Georgia, and share how car insurance premiums can change at different points in your life.

Age is one of the biggest factors that can affect the cost of car insurance in Georgia. In general, young drivers pay the most expensive rates and middle-aged adults pay the lowest rates. The average cost of car insurance is correlated to driving experience and risk levels, which is why newly licensed drivers often pay the highest rates.

As drivers get older, their car insurance premiums usually start to drop, assuming they maintain a good driving record and clean claim history. If you have a complicated driving history or have filed multiple claims in a short period, your car insurance premium could increase as you get older. Once claims and traffic violations fall off your record, rates should decrease once again.

While age is one of the most important factors that can affect car insurance rates in Georgia, there are many other factors that are also used to calculate your premium. To find the most affordable car insurance for your situation, it’s a good idea to compare rates. You can find cheap car insurance in Georgia using our online quote comparison tool.

Car insurance for teens in Georgia is typically very expensive. The average cost of car insurance for a teen driver in Georgia on their own policy is $7,401 per year. That’s 118% higher than the statewide average cost of car insurance in Georgia.

Teen drivers in Georgia pay extremely high car insurance premiums because they lack experience on the road. Newly licensed drivers are the riskiest to insure because they are more likely to make critical driving errors that can lead to serious collisions.

Data from the Centers for Disease Control and Prevention (CDC) finds that drivers between the ages of 16-19 have a higher accident rate than drivers in any other age group. To offset the increased likelihood of a claim, insurers charge higher rates for young drivers.

If you are the parent or guardian of a teen driver and you want to add them to your policy, you will most likely see your car insurance premium go up. Based on our recent rate data, the average cost of adding a teen driver to an existing car insurance policy in Georgia is $9,917 per year.

As the teen gets older and gains experience behind the wheel, your premium should decrease slightly. For example, you will likely see a bigger rate increase when you insure a 16-year-old driver and a smaller increase when you insure a 19-year-old driver.

To offset the rate hike when adding a teen driver to your policy, it’s important to take advantage of discounts, such as good student discounts, defensive driver discounts, or payment-related discounts. Some insurers also offer telematics programs that track driving behavior and reward safe drivers with more affordable premiums.

Adult drivers usually pay the lowest car insurance rates in Georgia. Our recent rate data shows that the average cost of car insurance for a 35-year-old in Georgia is $1,642 per year. That’s about 14% less than the statewide average for all drivers, which is $1,884 per year.

However, there are many factors that can affect car insurance rates for adult drivers in Georgia. For example, adult drivers who have a poor credit score will probably pay more than average for car insurance. Similarly, drivers who live in Atlanta or other urban areas will likely pay higher rates than drivers who live in more rural parts of the state.

It’s common for senior drivers in Georgia to pay slightly higher car insurance rates than middle-aged adults. As drivers get older, they are more likely to have impairments that can lead to driving errors and collisions. Due to the increased risk of insuring older drivers, insurance companies often charge higher rates for seniors.

As with middle-aged adults, keep in mind that the cost of car insurance for seniors in Georgia depends on many factors besides age. Some of the ways that senior drivers can lower their premium include taking a defensive driving course, bundling policies, maintaining a clean driving record, insuring a car with advanced safety features, and paying in full.

For most drivers in Georgia, car insurance rates start to go down around age 25. After this point, car insurance premiums usually decrease steadily over time, assuming the driver maintains a clean record and has no recent claims.

There isn’t a single cheapest car insurance company for senior drivers in Georgia. The cost of car insurance is personalized to each driver depending on factors like ZIP code, credit score, vehicle type, driving history, policy limits, and more. Seniors should compare rates from multiple different insurers to find the cheapest policy for their situation.

The average cost of full coverage car insurance for all drivers in Georgia is $1,884 per year, or about $98 per month. To compare, the U.S. national average car insurance premium is $2,049 per year. However, keep in mind that car insurance rates are different for everyone, so your premium could be higher or lower than average depending on your driver profile, vehicle, and coverage needs.

There are a variety of ways to lower your car insurance premium in Georgia. Many insurance companies offer discounts that can reduce your rate. Choosing a higher deductible can also lead to lower monthly payments. Having a good credit score and avoiding accidents and traffic violations will help you maintain a low rate overtime.

Car insurance companies determine how much they charge you based on your driver profile. Factors that can impact your rates include:

Read more about the factors that impact your car insurance rate

Switching your car insurance is easy, even if you are in the middle of your current policy.

Here are some helpful tips to consider to switch your car insurance:

The answer to this question depends on where you live and what you would like to cover.

Each state has its own minimum requirements on the type and amount of insurance needed. When you’re trying to determine what and how much car insurance you need, you can start by reviewing your state’s requirements.

Find out what’s required in your state

Once you review your state’s minimum requirements, you may find that you want additional coverage. For example, sometimes owners of new cars want comprehensive coverage to insure their car from natural disasters and vandalism, even though comprehensive coverage isn’t required by their state. To figure out what insurance you want, you can review the different types of insurance to decide what makes the most sense for your situation.

The biggest difference between Rate Retriever and other comparison sites is that we are a free and impartial research tool NOT an insurance marketplace. This means you can’t purchase a policy directly through RateRetriever.com, but you can use our tool to independently research your options and seamlessly connect with the provider you choose.

Unlike other insurance comparison sites, we:

We like to think that Rate Retriever is your insurance companion, not just another insurance comparison site. Our values guide everything we do, which is why we strive to offer transparent, trustworthy insurance tools.

There are many ways you can try to get cheaper car insurance. The first is simply to get quotes from multiple providers. This will help you determine if you’re currently receiving the cheapest rates based on your needs and driver profile. Rate Retriever makes the comparison process easy.

Sometimes, the reason your car insurance is so expensive is due to your driver profile. For example, drivers under 20 years old usually pay more for insurance than more experienced drivers, and drivers with a recent at-fault accident or traffic violation typically pay more.

There are ways to lower the cost of your insurance such as taking a defensive driving course. Check with your provider to see if there are any discounts you qualify for or can reasonably earn.

Rate Retriever works with national and local insurance providers to provide our users with a seamless insurance shopping experience. We may earn a commission from our insurance provider partners when you click on a link, call, or purchase a policy from one of the providers listed on our site. That said, we’re committed to providing you with accurate, bias-free information, and we do not allow our partnerships to limit the results or influence the information we share with you.

We do not sell your personal information, charge you for using our tools, or sell you insurance policies. Additionally, should you choose to purchase a policy from one of our partners, the price you pay will not be adversely affected.

![]() Kelsie Johnson

on

2024-04-15

Kelsie Johnson

on

2024-04-15

Georgia drivers must carry a certain amount of car insurance. Learn more about the state’s car insurance laws and minimum coverage requirements.